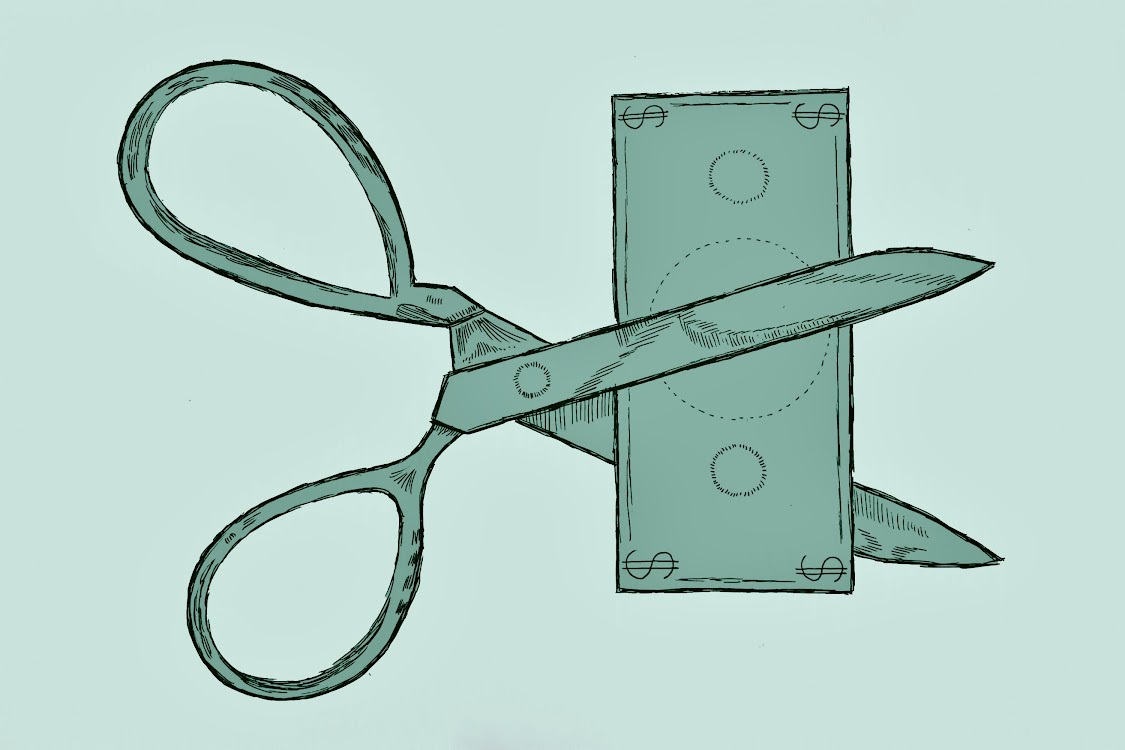

President Barack Obama recently announced his intention to expand Pay As You Earn, a student loan forgiveness program originally passed in 2012. The plan enables former college students who meet eligibility requirements to cap their monthly loan payments at 10 percent of their income, with those loans forgiven after 20 years. While this effort is a godsend for many, it is also shortsighted and only shifts the burden of this debt. Every forgiven loan must be absorbed somehow, and any true attempt to solve the burgeoning student loan crisis must attack the initial distribution of

those loans.

Outstanding student loan debt currently stands at more than $1.2 trillion. Of that, 14 percent is currently in default, a percentage only predicted to increase. Why are these numbers so high? Because tuition rates are skyrocketing, the job market is less than optimal, and student loans are so easy to receive. I distinctly remember signing my first UT loan. The process seemed so simple. Too easy. In just a few clicks, I had promised to pay thousands of dollars years ahead to an entity I could not visualize at a disturbingly high interest rate. The realization frightened me on impact.

I was one of the lucky ones because I understood how the process worked and I had been planning my college financing for several years, but many students are not so fortunate. A study conducted last July by the Federal Reserve Bank of New York, concluded that American households have a poor understanding of the student loan process, with less than half of the respondents comprehending the consequences for defaulting on loans, even among those who had taken out loans themselves.

The fact that so many students are oblivious when it comes to student loans is not surprising. Financing is not a required course in most schools, and many incoming college students know very little about loans. Students are offered far greater loans than they actually need, and without knowledge of compounding interest, they wouldn’t recognize the danger of accepting a greater loan. Once loan money hits a student’s bank account, it’s easy to lose sight of it as belonging to someone else. Between the studies and socializing that fill university life, a student can effortlessly glide through college without realizing that interest accrues on their loans even while in school. The consequences of default are surprisingly easy to remain unaware of, but wage garnishment, ruined credit and lawsuits are legitimate threats.

Investing in the financial education of incoming college students is the only way to truly attack this crisis. Sacrifices will have to be made. Some will delay school in order to save. Others, even out of school, will forgo saving for retirement or other investments in order to pay off their loans. However unsavory, this is our economy, and the only way to slow this bleed is to ensure that more students understand the true cost of that money only a few clicks away.

Johnson is a recent philosophy graduate from Fort Worth. He plans to pay off his final student loan before the end of 2014.