About two and a half months ago, I arrived at the 40 Acres bright-eyed and naive, as many high school graduates do. I was introduced to personal finance when I was handed a card upon my arrival at orientation. With this plastic rectangle, I could lavishly spend on whatever I desired. I ate three meals per day, bought souvenirs and still had funds leftover. With experiences like these, any college student can be tricked into believing that personal finance is easy. What a beautiful misconception.

Soon you realize that the three-day luxury escapade at orientation is finished. Cue the first tuition bill. Then, the housing bill. Next, the textbook receipts. That’s when you realize that playtime is over.

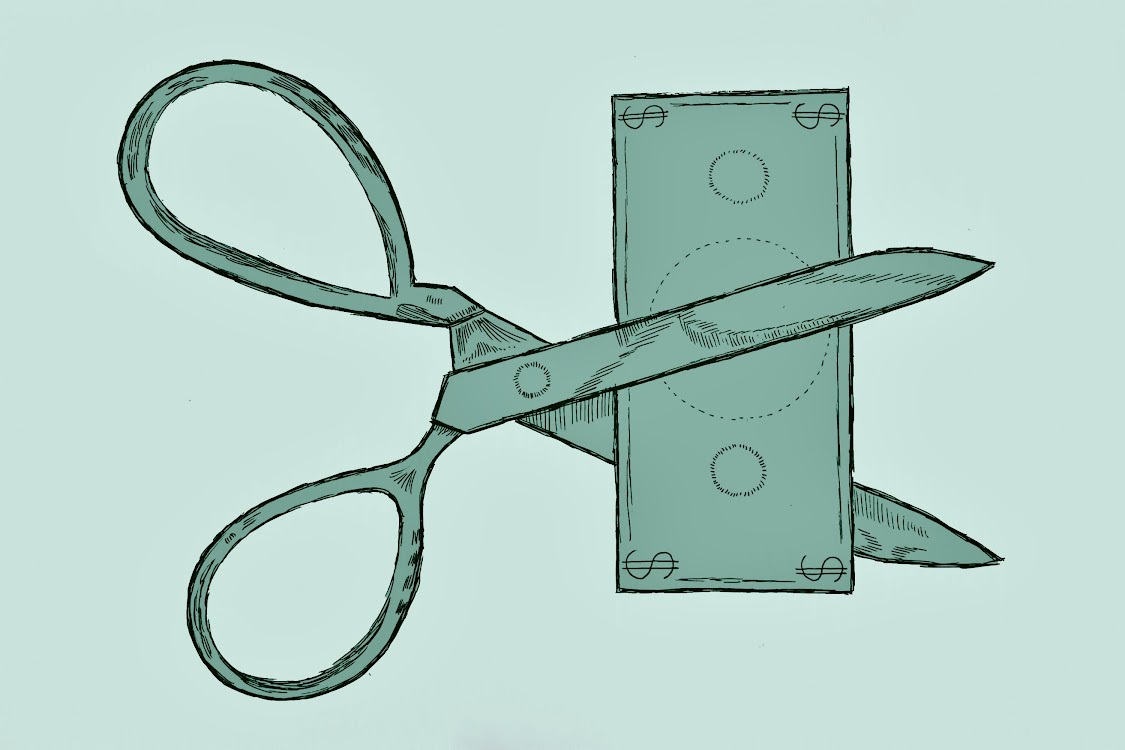

Unconsciously, students become discouraged from aggressively tackling their finances because of the looming shadow of interest rates and various service fees charged by different vendors. College does not have to be a time when we wait until our financial burdens are solved by paychecks in a far off future. It can be a time when we embrace the debt and tackle it head on by building our credit.

Credit score and an ability to pay directly affect your likelihood of securing loans for big purchases in the future. Increasing your score takes a while. It is crucial to start building credit now since a higher credit score helps lenders trust you with loans at lower interest rates. Tasks such as purchasing a car or a home require a high credit score to keep costs low. It would be a shame if you were so close to buying that dream home or fantasy car but could not be approved for the necessary loan.

Electrical engineering freshman Eric Chen has already taken steps to improve his credit.

“I’ve discovered that American Express and Discover are the easiest institutions to get started with,” Chen said. “They are generally easier to get approved for.”

The University Federal Credit Union is another institution available to Longhorns that aids in building credit. Students have the option of opening a secured credit card account that allows them to utilize a relatively safe way to start acquiring debts and paying them off immediately. And it’s on campus!

“Think of a credit card as a debit card with rewards,” Chen said. “It helps to stop you from thinking of it as an extension of your purchasing power.”

This way, we don’t spend more than what we have. Using credit cards only for regular purchases, such as groceries, is one way that we can circumvent the exponential growth associated with these types of borrowing.

Adulting does not begin after graduation. It begins now. When you think of where you’ll be in a few years, the odds that you’ll make a major purchase such as a car or a home are very likely. As you take responsibility for your finances for the first time, exercise good caution. Only borrow what you can afford, and pay what you can as soon as you can to mitigate paying interest. While institutions such as the UFCU may try to help you out, they can’t get rid of those rates altogether. This means you have to take some initiative and do yourself a favor.

Building good credit is one way that we can start building our finance in the face of potential debt. While you might be in the red, it helps down the road to take advantage of borrowing in the name of savings. Let’s give credit where credit is due.

Ancheta is a business freshman from Houston.