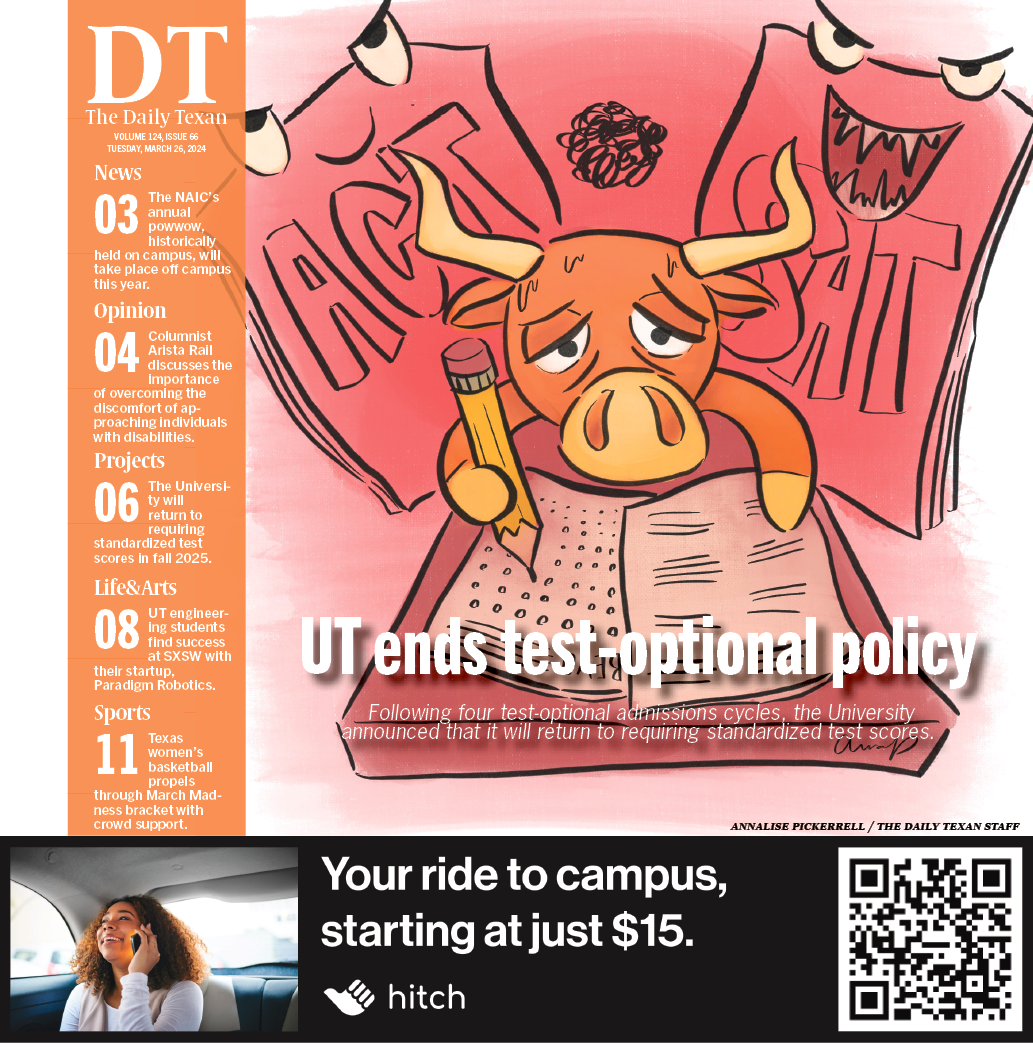

Authors of a recent Forbes article generated considerable buzz when they promoted a plan for the aggressive privatization of university services. While elimination of state political control may appeal to those put off by the latest rumors of the UT Board of Regents’ dangerous partisanship, sweeping privatization of our campus invites trouble.

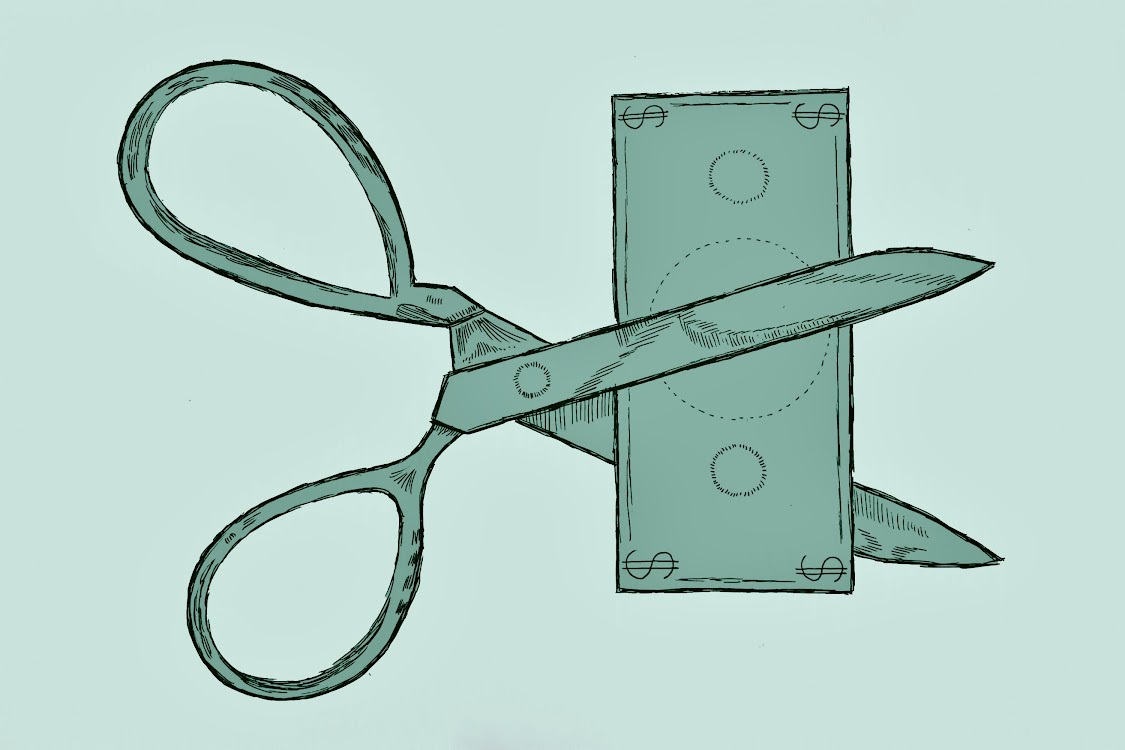

Successfully raising donations sufficient to compensate for the elimination of state funding is not the plan’s only hurdle. The predatory practices of the banks and financial firms that now hold contracts with almost 900 colleges and universities—including Arizona State University and Texas A&M University—demonstrate the dangers of excessive privatization.

The Boston-based U.S. Public Interest Research Group (PIRG) released a report last month that shed light on the complicated financial and legal issues inherent to universities’ relationships with banks and financial firms. Essentially, financial institutions offer schools incentives, including signing bonuses and direct payments, to privatize financial and administrative functions. The most basic partnerships allow a bank or financial firm to manage “closed loop” monetary functions of student ID cards. These systems, similar to Dine In Dollars or Bevo Bucks, turn student IDs into prepaid cards used to pay for on-campus services.

But most partnerships don’t stop there. Banks and firms are increasingly adding “open loop” functions that tie a student’s ID to his or her bank account and transform it into a debit card. In addition, students with accounts at their university’s partner bank can access financial aid funds more quickly than they could through another bank or traditional checks.

In order to withdraw those funds, however, students often have to pay an ATM fee. These transactions raise a difficult ethical question: Is it acceptable for banks and financial firms to charge students to access taxpayer-provided money? Certainly, any process that funnels tax dollars into corporate coffers should be thoroughly and critically evaluated.

Even more disconcerting, this system acts counter-intuitively by charging unnecessary fees to financial aid recipients, the students by definition least able to afford those fees. In addition to ATM withdrawal fees, many banks and firms charge per-swipe and inactivity fees, forcing students to pay regardless of whether they use their card or not.

The PIRG report also raises concerns about banks’ and firms’ deceptive marketing practices. A partner institution will often “co-brand” on student IDs, placing its logo next to the university’s seal or mascot. Many students register this as their school’s implicit endorsement of a particular bank, and automatically trust that bank more than its competitors. Some bank partners also gain the exclusive rights to table in common areas and give out “freebies” like sweatshirts or mugs. These strategies have the potential to turn naive college students into captive consumers, their choices influenced by what they see on campus and on their own IDs.

Some schools even force students to activate a card by refusing to disburse overpayment refunds, such as excess financial aid, through accounts at any bank other than their partner institution. Finally, PIRG speculates that some universities’ distribution of student information to banks violates the Family Educational Rights and Privacy Act.

On the bright side, the report notes that UT-Austin is the largest public university without such a contract. Jamie Brown, Department of Student Financial Services spokesman says UT decided not to partner with a specific bank because, “It doesn’t make sense for us to participate in these kinds of programs, especially if we’re trying to educate students on smart spending.” UT follows a traditional financial aid disbursement protocol. The University will either deposit funds directly into a student’s account, at any bank, or simply write the student a check. Although more conventional and less streamlined than a bank partnership, this approach remains the most ethical and straightforward method to distribute financial aid and overpayment refunds.

For most students, college offers the first opportunity to manage their own finances. University-bank partnerships discourage smart shopping and responsible financial practices by limiting choices and normalizing excessive, unfair fees. More universities should follow UT’s example by resisting financial incentives that come at the expense of following through on their responsibility to students.